Summary

- Embedded finance is no longer just a fintech buzzword; it’s a business imperative for enterprises.

- Highlights the industries being transformed by these embedded offerings.

- Breaks down the 3-layer technology stack that powers embedded finance.

- Share real-world examples showing how these solutions deliver results.

- Get a practical playbook to help enterprises get started quickly.

What if your enterprise didn’t just use financial services, but became one?

JPMorgan Chase and Walmart just proved it’s possible. Their joint embedded finance solution handed marketplace sellers integrated payments, lending, and cash management, all inside a single platform. No bank. No redirect. Just finance, built right in.

And they’re not doing it to be clever. They’re doing it because the numbers demand it. The embedded finance market was at $146.17 billion in 2025, and it’s sprinting toward $690 billion by 2030 at a 36.41% CAGR.

The World Economic Forum puts the broader opportunity at a staggering $7 trillion.

Here’s what that really means for your enterprise: your customers are done switching platforms to complete a financial action. They want payments, loans, and insurance to happen exactly where they already are. Your enterprise could be that one-stop solution, the platform they never have to leave. That’s not just a feature. That’s a business model.

The businesses winning right now aren’t waiting for a bank to hand them the future. They’re building it through smart, strategic fintech software development. This blog breaks down exactly how.

Accelerate your fintech vision with trusted tech experts.

Connect NowWhat Embedded Finance Means for Enterprises

You’ve seen it: “Buy Now, Pay Later” options or ride-sharing apps with built-in payments, no switching apps, no friction. For enterprises, embedded finance means integrating payments, lending, banking, and insurance directly into the platforms your customers already use.

Key Embedded Finance Features for Enterprises

- Banking & Accounts: Branded accounts, digital wallets, virtual accounts

- Card Issuing: Payout and expense cards

- Lending: Invoice financing, merchant cash advances, PO funding

- Insurance: Transit/cargo, liability, trade credit, product warranties

- Revenue & Compliance: Tax automation, payroll, KYC/KYB checks

- Investing: Micro-investing, crypto trading

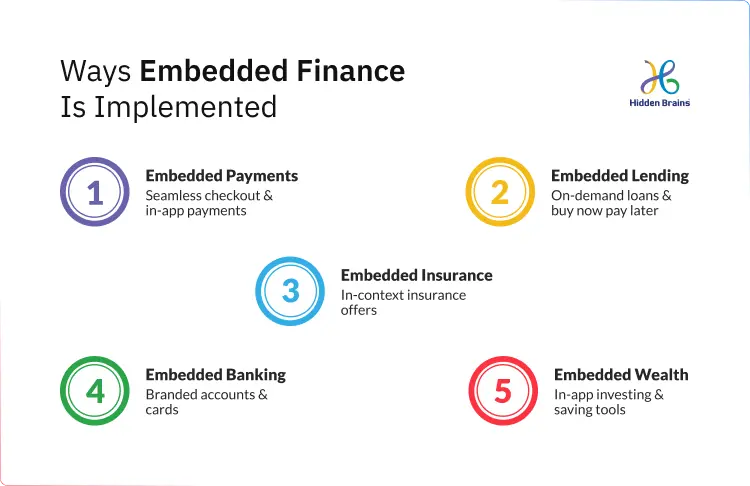

Key Ways Embedded Finance Is Implemented

Embedded Payments

The most common entry point. Payments are integrated directly into the product experience, at checkout, within a marketplace, or as part of a service workflow. No redirects, no third-party payment pages. Just a clean, native transaction. Stripe, Adyen, and Braintree are enabling this at a massive scale.

Embedded Lending & BNPL

Enterprises offer credit or Buy Now Pay Later options at the exact moment a purchase decision is made. Shopify Capital lends to merchants based on their own platform data. Klarna embeds financing at checkout. The result: conversions go up, and enterprises earn from interest and fees without touching the core banking stack.

Embedded Insurance

Tesla offers auto insurance at car delivery. Travel platforms offer trip insurance mid-booking. The product becomes the insurance distribution channel, and customers get contextual coverage without hunting for a policy. Platforms like Codat and Walnut are making this API-accessible for any enterprise.

Embedded Banking (BaaS)

Banking-as-a-Service allows enterprises to offer branded banking products, accounts, cards, and wallets without a banking licence. Unit, Green Dot, and Railsr are powering white-label banking experiences for non-bank brands. Your platform can hold funds, issue cards, and manage accounts, all under your brand.

Embedded Wealth & Investments

HR platforms are starting to offer in-app investment accounts and automated savings tools. Payroll platforms offer instant access to earned wages. The financial product becomes a retention feature and a revenue line, baked into the enterprise SaaS experience.

Each of these implementation models runs on one thing: smart software development for fintech. The kind that bridges your business logic with financial infrastructure, seamlessly.

The 3-layer Tech Stack Powering It All

Here’s the thing about embedded finance that most people do skip: it only works if the architecture underneath it is built right.

Get the stack wrong, and you’ve got compliance nightmares, failed API calls, and a user experience that drives customers straight to your competitor.

Here’s the 3-layer model that makes it work:

Layer 1: Infrastructure Layer

- BaaS providers (Unit, Synapse, Green Dot, Railsr)

- Core banking APIs and ledger systems

- Cloud infrastructure (AWS, GCP, Azure) — built for scale and regulatory compliance

Layer 2: Integration & Orchestration Layer

- RESTful & GraphQL APIs connecting financial services with your enterprise platform

- Event-driven architecture (Apache Kafka, webhooks) for real-time data flows

- KYC/AML compliance engines and identity verification SDKs

- Payment orchestration platforms (Stripe, Adyen, Braintree integrations)

- Fraud detection and risk scoring systems

Layer 3: Product & Experience Layer

- White-label financial product UIs, wallets, dashboards, loan flows

- AI-powered credit scoring and personalization engines

- Real-time analytics, notifications, and reporting tools

- Mobile SDKs for seamless in-app financial experiences

Most enterprises focus on Layer 3, the shiny product surface. But the real magic (and the real risk) lives at Layer 2. The orchestration layer is where expert fintech software development separates a seamless embedded experience from a broken one. It’s the layer that decides whether your financial product feels invisible or impossible.

Real-world Examples & Key Use Cases by Industry

Theory is useful. But proof moves people. Here’s what embedded finance looks like when it’s done right with software development in finance:

Payments

Uber pays drivers instantly inside the app, no bank transfer, no delay. Stripe powers checkout financing for thousands of ecommerce businesses.

The result: faster settlements, higher conversions, and a financial experience so smooth that users don’t even notice it.

Credit Intelligence & Risk Infrastructure

Saudi Arabia’s national credit bureau was running on blind, legacy systems, manual workflows, and no real-time risk visibility.

Hidden Brains rebuilt the entire stack: microservices architecture, automated data pipelines, real-time credit monitoring, and portals for consumers, corporates, and partners. 62% revenue growth, 94% user satisfaction, 700+ financial institutions now benchmarking against it. Credit intelligence stops being a back-office report and becomes a live, always-on risk engine.

Lending & BNPL

Ant International embedded working capital loans for SMEs directly inside their marketplace credit delivered at the exact moment it’s needed. HSBC’s SemFi brought trade financing inside B2B platforms. No bank visit. No application delay. Just capital, in context.

Insurance

Tesla offers auto insurance before the car leaves the lot. Walnut enables any SaaS platform to offer contextual coverage through a single API. Insurance stops being a follow-up email and becomes a built-in product feature.

Banking-as-a-Service

Green Dot’s Arc and Railsr let enterprises offer branded accounts, cards, and wallets without a banking licence. Full financial product suites, launched in weeks, not years, entirely under your own brand.

How to Make Winning Moves- The Fintech Development Playbook

Strategy without execution is just a slide deck. Here’s the crisp playbook for enterprises ready to actually build:

- Define Your Use Case First

Start with one financial product: payments, lending, or insurance. Build depth before breadth. - Choose a BaaS Partner, Don’t Build the Infrastructure

License it. Your edge is the experience, not the core banking stack. - Build the Integration Layer with Intent

APIs, compliance, and orchestration are your competitive moat. Don’t cut corners here. - Design for Invisibility

The best embedded finance is the kind the user barely notices. UX is everything. - Nail Compliance From Day One

KYC, AML, PCI-DSS, GDPR, build it in, not on. Retrofitting compliance is expensive and slow. - Data Drive Iteration

Embedded finance generates rich financial data. Use it to personalise, optimise, and grow.

Specialist software development for fintech gives you an edge, creating scalable, compliant, and high-converting architecture that keeps users engaged within your platform.

The Future of Embedded Finance: 4 Ways It Will Change Fintech

We’re not at the end of this story. We’re barely at the beginning. Here’s where it’s going:

AI-powered Hyper-personalization

Embedded finance will use real-time behavioural and transactional data to offer hyper-personalised credit limits, insurance premiums, and investment products delivered at the exact moment a customer needs them. Finance that anticipates you. That’s where this is headed.

Real-time Cross-border Payments

With ISO 20022 adoption maturing and Central Bank Digital Currencies (CBDCs) moving from pilot to production, embedded cross-border payments will become instant, cheap, and invisible. Legacy SWIFT flows for SMEs? Gone.

Embedded Finance in Every B2B SaaS Platform

Every enterprise SaaS platform, HR, ERP, and CRM will embed financial products. Payroll platforms will offer instant wage access. ERP systems will offer supply chain financing at the point of purchase order creation. Finance becomes a feature, not a department.

RegTech Fusion

Compliance will get embedded, too. AI-driven RegTech will handle KYC, AML, and fraud detection in real time, cutting compliance costs by up to 40% and removing human bottlenecks from financial onboarding. The regulatory burden gets lighter. The speed gets faster.

Embedded Finance: The Future of Seamless Payments

Embedded finance is just getting started, and its potential is enormous. Consumers and businesses alike are demanding financial services that meet them where they are, the platforms they already use. Not only in a bank branch, but also on a separate website or app. It’s beyond all of that.

The market is responding quickly. Embedded finance is reshaping how payments and financial services are delivered, creating seamless experiences that put users first.

What’s even more telling is who’s driving the growth. It’s not just consumer fintech startups. It’s enterprises, B2B platforms, logistics companies, healthcare networks, and manufacturers that are embedding financial capabilities into the operational tools their teams use every day. This is a B2B-first revolution, and it’s happening right now.

This isn’t a fintech trend. This is a fundamental restructuring of how financial services are delivered, and the enterprises that move now will define the landscape for the decade ahead.

The window to move first is open. And it’s the right time to choose software development for fintech.

The market won’t wait. Neither should you.

Let’s Talk

Turning Embedded Finance into Reality With Hidden Brains Expertise

Embedded finance is working, and the winners are already ahead. Don’t sit on the sidelines.

At Hidden Brains, we are your go-to partners. We build financial infrastructure that enterprises can trust, infrastructure that scales, complies, and converts from day one.

Here’s what we focus on in every embedded finance engagement:

- Domain-first thinking: We understand fintech compliance and financial architecture, not just the code that powers them.

- API-first architecture: Every solution is built for seamless integration, flexible scaling, and long-term adaptability.

- Security & compliance by design: PCI-DSS, KYC/AML, GDPR, embedded from the very first sprint, not retrofitted later.

- End-to-end delivery: From BaaS partner selection to UI polish, we own the full stack, so you don’t have to manage five vendors.

- Proven enterprise experience: We’ve built for high-growth startups and enterprise-grade platforms alike. We know the difference, and we build accordingly.

Whether you’re a startup with a bold fintech idea or an enterprise ready to embed financial products into your core platform, we have the team, the process, and the track record to get you there.

Frequently Asked Questions

Think fintech software development is complicated? Our experts have the answers to simplify your process and help you move ahead with confidence.

How do we integrate embedded finance into an existing enterprise platform without disrupting current operations?

The right approach is API-first and modular. You don’t rip and replace; you layer financial capabilities onto your existing infrastructure through well-architecture APIs and middle ware. A phased integration starting with one use case, like payments or lending, mini-mise disruption while delivering early value.

What compliance and security obligations does our enterprise take on when embedding financial services?

Your obligations depend on the financial product and the markets you operate in. At minimum, expect KYC, AML, PCI-DSS, and GDPR requirements. The good news: with the right BaaS partner and a compliance-first development approach, much of the regulatory infrastructure is inherited, not built from scratch.

How do we evaluate and choose the right BaaS partner for our embedded finance strategy?

Evaluate on four dimensions: regulatory coverage in your target markets, API quality and documentation, financial product breadth, and SLA reliability. At Hidden Brains, we are your guide who walks through from strategizing to infrastructure and post-implementation.

Can a startup realistically launch an embedded finance product without a large development team?

Absolutely. Modern BaaS platforms and fintech APIs are built for lean teams. With the right development partner handling architecture and compliance, a startup can launch a focused embedded finance product, such as payments, BNPL, or insurance, in as little as eight to twelve weeks.

How much does it cost to build an embedded finance solution?

Cost varies significantly by complexity. A basic embedded payments integration starts at a fraction of what a full BaaS product costs. The smarter question is: what’s the cost of not building it? Startups that embed finance early build a revenue stream and stronger customer retention at the same time.

Do we need a banking licence to offer financial products on our platform?

No. Banking-as-a-Service providers like Unit, Green Dot, and Railsr hold the licences. You build the product experience on top of their infrastructure, under your brand, inside your platform, without the regulatory overhead of becoming a licensed financial institution.

What role does AI play in making embedded finance products smarter over time?

AI powers real-time credit scoring, dynamic fraud detection, personalised product recommendations, and automated underwriting. The more transaction data your platform generates, the smarter the models get, creating a compounding advantage that generic financial products simply can’t replicate.

Conclusion

The market is moving, and embedded finance is one of the most significant opportunities enterprises have right now. From insurance and lending to payments and full banking experiences, the financial layer is shifting from a separate destination to a native part of every platform. The enterprises investing in this today aren’t just adding features; they’re building the platforms customers never have to leave. The window is open. The infrastructure exists. The only question is whether you’re building or watching.